SP8DE

THE GAME OF CHANCE CHANGED A DECENTRALIZED PLATFORM FOR GAMING DAPPS

Introduction

Welcome to Spade, a blockchain-based platform capable of supplying unbiased public randomness for developing and running distributed casino applications. Spade is designed to suit the purposes of all the actors comprising the online casino landscape and as such represents the new breed of digital institutions, a distributed intermediary.

The spark that lit this project and continues to inspire us now, is that early blockchain and Bitcoin casinos simply didn’t get it right. The Blockchain community was younger and wilder, ideals of distributed freedom were burning brighter… still, early adopters who applied blockchain technology to gambling promoted the wrong ideals; those undermining the image of decentralized casinos. Instead of promoting transparency and cost efficiency that characterize blockchain technology, they promoted anonymity and cyber anarchy. Instead of making the casino for everyone, they kept it to themselves.

By no means are we here to judge. Instead, we are here to change. We do not say that old ways are bad, but can prove that new ones are better. We hold faith in the decentralized future and appreciate the charm of gambling.

We soon realized that there is only a fragile wall of glass between the old centralized gambling and the future global distributed casino. This is it, a simple yet captivating idea. The future is here: we can run a zero-house edge decentralized casino with close-to-zero transaction fees and provably fair random numbers feeding entropy into a myriad of Smart-Contract-based open source casino applications that can be developed by anyone who has a worthy idea by means of state-of-the art application-specific as well general-purpose programming languages. “We can” was the silent voice of the idea. Now it is the marching echo of “we do”.

As it frequently happens, technological progress made a massive leap forward that went unnoticed by the majority of human kind: people still prefer the traditional narrow-minded and boring online casinos that set draconian house edges and cannot be proven fair. Once again, no one has the right to judge: it is just an existential business need, produced by a dilapidated business model and an inch of greed.

Worse than this, however, is that even the enlightened ones, those chosen to witness the dawn of the distributed world have noticed a perfect fit between distributed consensus protocols and gambling applications, have synthesized them and… nothing. Some of these projects got infamous due to money laundering accusations, some have spoiled the beauty of the idea by running centralized online casinos and simply allowing for cryptocurrency deposits, others got their moments of fame during TGAs, today, however, few can recall even the names of these projects. Of course, there are some notable exceptions to this rule, but while succeeding locally all these projects have failed to create awareness. None of them has broadcasted the essential message: “There is no glass wall; the future of gambling is now; we are better in every single quantifiable aspect; if quantifiable is not enough, we also have the powerful idea of the distributed future, while those who are stuck in the past have only a couple of servers and an unaudited poker protocol”.

We will do what no one has done before. Spade is a blockchain-based platform for developing distributed gambling applications. As a platform for gambling applications with self-respect, we are equipped with the protocol for generating fresh unbiased public randomness. As a team with some aspirations we have it provably fair and completely decentralized. We feel that it is important to be true to the spirit of the venture we embark upon: if blockchain is the universal and undisputed source of truth then it should also be the broadcast channel for randomness. We think that single points of failure should be perceived by anyone as just a relic of the past. This feature, while setting us aside most starkly, is only a part of what we have to offer in terms of technological

WHAT IS SP8DE

Sp8de is a protocol for blockchain-based platform with multiple features that are essential for the growing blockchain gambling industry and whose solid implementation is lacking in any of the currently existing projects in this space.

vision SP8DE

In the European Union the online gambling industry grew nearly 19% from the first half of 2015 until the first half of 2016. The casino industry in particular generated over US$2 billion in revenues during this period. It is expected that until 2020 this number will reach US$2.25 billion per year representing about 12.5% revenue growth [1]. In the US for the period 2015 until 2016 online casino revenues increased by 24.4% and are expected to reach US$4 billion by 2020 [2]. The EU and the US are just a small part of the worldwide casino industry. Globally, the projections of the online casino show that for the period 2017–2025 the market will experience growth of about 130% reaching US$97 billion with cumulative annual growth rate of nearly 11%. Currently over 6 million adults are officially participating in gambling activities around the world with projections of reaching 10 million by 2020 [3].

Since inception, the blockchain technology was the subject of close attention by gambling enthusiasts. Recent news from The Merkle [4] show how popular online Bitcoin betting has become. In aggregate the wagers put on online Bitcoin casinos in February 2017 have reached nearly 3 Bitcoin per minute. The price of Bitcoin at the end of February was about US$1,200 while now it is US$5,900 (approximately 292% growth) which means that as of today almost US$715 million worth of Bitcoin was gambled in February alone.

Bitcoin vs The Online Gambling Industry

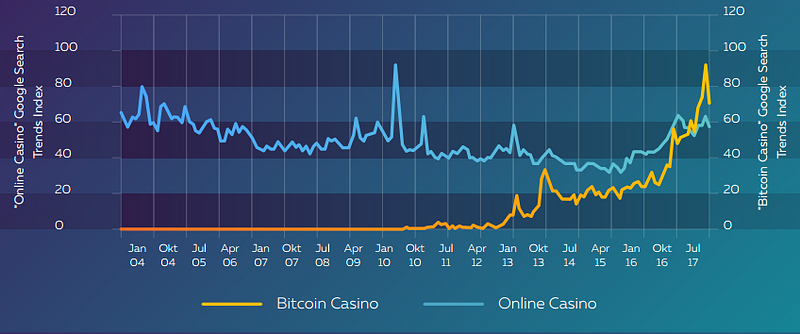

“Bitcoin Casino” vs “Online Casino” Popularity

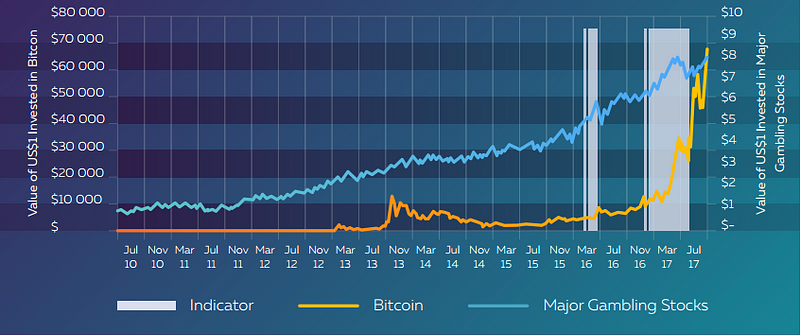

In Figure 1 we show how an investment of US$1 would have developed from 2010 until 2017 if it was invested into the giants of the online gambling industry1 [5] as compared to the same dollar being invested in Bitcoin. Apart from the fact that this investment in BTC would have provided US$70,502 as compared to only $US7.37 when invested in the index, one major observation can be made: the shaded areas show that as the Bitcoin blockchain technology was becoming more and more popular (that is the price of Bitcoin was rising) the traditional online casinos have also gained steam. However, when we look further in Figure 2 (Google Trends search for “Bitcoin Casino” and “Online Casino”) we see that the popularity of online casinos has been relatively stable and slowly declining since 2004. Only since the beginning of 2016 when the Bitcoin casinos have started to gain wide popularity did the online casinos see slight increase in interest. In addition, the search “Bitcoin Casino” has skyrocketed since May 2017 when it surpassed the search term “Online Casinos”. Furthermore, we know of the existence of at least ten relatively sound blockchain-driven casino projects that have entered the industry through a successful TGE and are still being developed. Although somewhat broad2, this overview points out to an important pattern which holds a lot of relevance for the future of the gambling industry.

Currently, online casinos seem to be only weakly affected by the growth in the interest in Bitcoin gambling and the blockchain-based casinos that at the moment appear to at least complement traditional online gambling. However, this is happening at a staggering pace and the tendency shows a possibility of blockchain-based gambling taking over online casinos. If the current pace of technological advancement of the blockchain industry is sustained, soon there will be no benefits left for the consumers in the more traditional online casinos.

1 To form this index, we create an equally-weighted portfolio of 888 Holdings, bet-at-home.com, GVC Holdings, Ladbrokes Coral Group, and MGM Resorts (although Bitcoin is traded during the weekends and holidays we only consider trading days). 2 When replacing “Online Casino” with “Online Gambling” the results are similar. Also replacing “Bitcoin Casino” with “Blockchain Casino” does not alter our results significantly. The results of searching “Ethereum Casino” are also similar to those of searching “Blockchain Casino”. Nevertheless, one has to consider that it is possible that people searching these keywords did not look for actual blockchain-based casino but rather that they want to gamble cryptocurrency such as Bitcoin.

The Blockchain and the Casino

In what follows we describe a protocol for decentralized blockchain platform for developing casino applications with multiple unique features whose solid implementation is lacking in any of the currently existing projects in this space. The concept of decentralized consensus that lies at the heart of blockchain is based on the smart application of cryptography and game-theory. Combined, they create the economics of trust and hold immense potential for revolutionizing many classic industries.

This backbone of blockchain technology renders it an obvious candidate to consider in developing online gambling applications as, arguably, trust considerations and the need for transparency are — and always used to be — two major cornerstones of the gambling industry [6], [7], [8], [9]. In particular, blockchain has the potential to provide transparency to all transactions, drastically reduce the house edge, nearly eliminate transaction costs, ensure anonymity of participants and ultimately, create the trust among players and other industry participants. This rapidly evolving technological stack offers immense potential for improvements in the online gambling space, however, it also carries multiple new pitfalls that are scarcely (if at all) researched and poorly understood. To understand the benefits the blockchain brings, one needs to delve deep in the economics of casinos (the institutional viewpoint). Appreciating the challenges requires an overview of the mechanics of the blockchain technology.

Economics of Gambling: An Institutional Perspective

While being driven throughout its long history by complex economic and sociological changes, the gambling industry has dramatically changed its competitive and institutional landscape — on the supply side it has changed remarkably little from the perspective of a person who wishes to try one’s luck. Indeed, it is still the same set of games that dominates the casino landscape, it is still the chance that defines one’s faith and these are still the classic transaction costs that interfere into the process, owing to the fact that the world we live in is not frictionless.

It follows that we can view the casinos from the perspective of institutional economics, a branch of economics studying the impact of institutions on the behavior of economic actors.

One of the major roles the financial institutions play, in modern economics, is economizing on transaction costs, thereby facilitating financial transactions that would otherwise be unfeasible. They also serve as escrows, notorious trusted third parties, who facilitate trust among the participants allowing them to enter into an exchange more efficiently than would otherwise be the case [10].

In this vein, casinos act as “gambling” intermediaries realizing the economies of scale, maintaining order and quality of service, thereby facilitating the “conditional” transactions — bets.

Let’s imagine the evolution of the gambling industry as a path towards reducing the transaction costs where innovative industry newcomers attempt to take a piece of the overall pie from the old incumbents by bringing gambling closer to the frictionless ideal.

In this vein, classic casinos reduce security and search costs, facilitate standardization by using chips and having house rules and, most importantly, realize economies of scale by bringing together people united by the shared desire to gamble. Following this line of reasoning, online casinos while performing the same functions as their classic brick-and-mortar counterparts, also facilitate convenience and economize on the travel costs on the

side of players. The major reason for their existence, however, stems from their more lightweight cost structure that is characterized with virtually zero marginal cost of adding a new client. This translates into significantly lower overhead costs, results in smaller house edge and, therefore, smaller average wagers and larger average net gains on the side of the clients.

The advent of the cryptocurrency casinos came as a result of their anonymity feature as well as absence of any regulatory oversight. As many other applications of the blockchain technology in its early days, the major considerations behind setting up casinos on the blockchain were idealistic, impractical or outright shady in nature. The anonymity and laissez-faire regime, however, are not the features that fit best into our line of reasoning: indeed, the decentralized infrastructure does not imply any server maintenance costs: the protocol is autonomous; the bets are fair: the protocol code is public; its workings are imprinted into the immutable ledger forever and can always be verified by anyone.

As a rule, once something new offers better ways for solving old problems, there always is a catch

The Mechanics and Issues of On-Chain Casinos

Summarizing, the blockchain revolution allows for greatly enhanced transparency and efficiency of transactions, levels the playing field for online game development and greatly reduces overhead costs erasing the necessity of maintaining relationships with trusted third parties, bringing the concept of online casinos to a completely new level.

While being clearly beneficial in some aspects, the net benefits of blockchain to the general public willing to put their hard-earned funds on stake are less clear-cut. The reason is that, unfortunately, while being secure and trustless, not a single blockchain protocol can compete in terms of efficiency with centralized systems, such as those that are used by the off-chain online casinos nowadays.

This imposes heavy burden on the user experience: one can imagine the winner’s frustration caused by the necessity to wait for 10 minutes before knowing if the roulette round actually settled on the blockchain. Even a 10-second delay can be detrimental to user experience once certain types of online gambling applications are concerned3.

Ordering of transactions is of paramount importance in a distributed ledger (the root of the double-spend problem). Unfortunately, simple time stamping cannot be used to achieve distributed consensus on the ordering of transactions in a decentralized peer-to-peer network. The blockchain protocols were created instead, offering a successful solution to the issue. However, decentralization always comes at a cost. Each block needs time to be mined and this creates inherent delays that are detrimental to user experience as far as casino applications are concerned4. Therefore, the first problem that needs to be resolved as efficiently as possible before online casinos can migrate on-chain is transaction settlement times.

The second inherent problems lie around transaction fees. Indeed, all the praised benefits of the decentralized payment networks, such as instant settlement and virtually absent transaction fees turn their back on those daring to employ them for micro-transactions. For example, currently the transaction fee to send ether on the 3 For example, an online casino (NetEnt) has been heavily criticized by its community for having a delay of less than 300 milliseconds (0.3 seconds) in knowing whether they won or lost; and delaying the withdrawal of big winnings (e.g. jackpot) has been famous in the industry. A simple search in Google “online casino delay” yields nearly 1,000,000 results, indicating how prevalent delays in online casinos are and how frustrated the online gambling community is with them.

4 This, of course, only applies once there is a fundamental limitation on the amount of games that can be played in every block. In currently existing applications, there indeed is such limitation — and it’s 1. For as far as the block content is a required input for generating randomness, one game outcome is produced for every block.

native Ethereum blockchain is about US$0.351 and sometimes over US$1. Such fees are game stoppers in a literal sense when it comes to for example, 5-dollar bets [14], [15]. No one would accept 20% brute transaction fees for a US$5 online bet. This problem is further exacerbated by the fact that most of the popular blockchains currently in existence are based on Proof-of-Work consensus protocols that are infamous for not scaling too well. This implies that soon we can and will witness situations where a gambler would have to either pay even higher transaction fees or experience large delays in settlement (see problem 1). It is also not clear, how to incorporate such choices on the level of the gaming application with more than one party involved. Furthermore, given that transaction fees on Ethereum or Bitcoin blockchains are paid in the underlying virtual currency, the cost of transaction is actually directly tied to the price of this currency.

This translates into a proportional increase in transaction costs. Therefore, an ideal solution for an on-chain casino would necessitate a protocol that can scale seamlessly and that would have low transaction fees. This is, however, far from being the end of the wish list when it comes to blockchain casino applications. Here we have approached the cornerstone topic in on-chain casino design. The immanent importance of this topic can only be matched by the extent of controversy associated with it. Before delving deep into complexities of probability theory, let’s summarize what has been said so far

The uprising of the casino industry from the early days of humanity until the very end of the XX century can be portrayed in standard outlines of economic theory: it has been a long quest towards erasing the transaction costs by the means of centralization and institutionalization of the gambling process.

The problems that have remained unresolved included poor transparency, high overheads incurred by casinos to maintain lucrative buildings and other required infrastructure that translated into high house edges; and, finally, the need to travel to a “physical” location.

An additional problem was that of inclusion: indeed, not everyone could participate in the development of new games. Some of these problems have been partially resolved by the slow migration of casinos online. Nevertheless, those of poor transparency and large house edges have also remained. In general, these are the problems that are inherent to the legacy financial system; the one based on intermediation and trust.

Therefore, it comes as no surprise that numerous projects have embraced the challenge to move the gambling process on-chain. This, however, turned out to be an ambitious aspiration with numerous pitfalls and seemingly unsurpassable technological barriers. While resolving the issue of inclusion, transparency (from the gambler’s perspective) and excessive house edges, blockchain gambling exacerbated those of high transaction fees and anonymity. It also brought new challenges along with it: how do we resolve the issue of slow settlement?

Finally, we addressed the sinle most important problem: the generation of the distributed randomness.

Indeed, how does one generate provably random numbers on-chain? Overall, how one achieves provable randomness in applications where multiple parties are involved and the random number generated determines the distribution of the monetary gains and losses for those involved? An easy solution would be to use a local source of randomness, such as RAND() function in Microsoft Excel©. However, there is a problem with this approach that renders it inefficient: local sources of randomness can be easily subverted and thus, there is no easy way for all the parties to verify that the number provided by a party is the number actually generated.

What about public sources of randomness? For example, Random.org, NSA or NIST all serve to provide “pure” randomness which is sampled from various natural sources, such as quantum physics processes. While indeed being public and random, these sources of random numbers suffer from all those problems we inherit from the ‘centralized’ yesterday: any application, however distributed, relying on them automatically raises the ‘single

point of failure’ red flag. Their outputs are susceptible to human errors, present an adversary with incentives to undermine their workings and finally, give malicious incentives to those running these protocols.

As always, when one is stuck being unable to find a theoretically convincing and practically appealing answer in the domain of centralized applications, the world of distributed consensus is the place to search for answers. There is no easy way to get distributed randomness: blockchain protocols are deterministic by nature and, do not have implementations of random number generation on the protocol level. But it wouldn’t be blockchain if this was the final answer. The following ‘solutions” have been proposed and implemented:

- Most of the attempts to circumvent this limitation in the end still rely on fresh entropy provided by either the users themselves or random oracles that in turn can either be manipulated or have malicious incentives of their own. So, random oracles — off-chain — single point of failure — red flag.

- Others opted for a different path and proposed using the block hash. While such protocol design is much more appealing from a theoretical viewpoint as it generates random numbers on-chain (no red flag), it has another major flaw: given sufficiently large monetary incentive miners with sizeable hashing power can manipulate the game outcome by not submitting the freshly mined block. Using timestamps and virtually any other block content falls victim to the same issue.

- Commitment schemes: the most promising solution with two major drawbacks: huge computational overhead and possibility that a malicious player will not open the secret after learning the outcome of the game. In other words, these schemes lack guaranteed output delivery. Monetary disincentives can be introduced to punish malicious actors basically collateralizing the Smart Contract thereby forcing the output delivery. In theory it works just fine. In practice one ends up with a slow and terribly expensive working protocol with limited applicability.

As we will show, something that is effective but inefficient can always be improved, but not the other way around. Points 1 and 2 unfortunately belong to the latter category, but the situation with the commitment schemes is different. The discussion so far has been quite abstract. A legitimate question is what does it all mean for the distributed gambling applications? Let’s review the recent projects in this sphere that have received their part of public attention.

The Mechanics of Spade

Spade is the new-generation blockchain-based gaming platform aimed at all the participants of contemporary casino ecosystem. We call it “new-generation” as Spade satisfies all the aforementioned conditions of a ‘proper’ blockchain casino. We build Spade on top of the blockchain called Cardano. The Cardano project itself is a monumental work that embraced the best practices and most far reaching innovations in the area of cryptocurrencies and packed them into a single state-of-art system. It is being developed and maintained by a large team comprised solely of PhDs in the field of programming and cryptography, and experienced engineers.

In what follows we will illustrate how Spade provides an environment for the design of gambling applications which are characterized with:

- Close-to-absent transaction fees and Proof-of-Stake powered scalability that is beyond the reach of any other on-chain casino protocol currently in existence;

- A mechanism to generate decentralized provenly uniform randomness at arbitrary time-spans;

- Provides rich Smart Contract functionality that allows for creativity in game design that is bounded solely by the fantasy of the developer (and the demand for the resulting product of course);

Fairness of the outcome is essential for gambling; it is the core.

Spade utilizes Cardano to design its ecosystem and thereby solves the problems normally associated with the on-chain casinos described above. Here is how:

- Transaction fees and scalability: the size of transaction fees is normally a function of the degree to which a given distributed system scales. Scalability can be defined as the relation between system resources and the number of nodes. Scalable systems gain in efficiency as new nodes join the network: BitTorrent and IOTA protocols are two prominent examples. Proof-of-Work based blockchain systems do not scale by construction: indeed, maintaining a common ledger implies every node possessing a full copy of this ledger. Without this condition, the security — most important property of such systems — is compromised. Therefore, there is no gain in efficiency when a new node joins the network. Ouroboros is a Proof-of-Stake protocol, meaning that at any given time, a trusted set of nodes maintain the integrity of the system. This protocol was shown in an experimental setting to be resistant to a handful of attacks that are known to plague other systems and are directly relevant to gambling protocols.

- Random number generation: finally, Ouroboros, the POS protocol underlying Cardano blockchain in its workings fully relies upon generating unbiased (i.e. uniformly distributed) entropy. The beauty of the idea is that the blockchain itself serves as a broadcast channel: the uniform randomness is generated on-chain! For us, this is the crucial point, so let’s elaborate on it further. POS systems are heavily dependent on the ability to generate good-quality randomness “to inject pure entropy into the system”. Without it, the integrity of the protocol can be interrupted. This stems from the fact that if there is a way to manipulate the process of selecting an agent who is chosen to validate the next block, an adversary can bias the election process. This is the root of the infamous “Nothing-at-Stake” problem and invalidates the whole concept of POS-based distributed consensus protocols. Apart from provably random number generation, another pre-condition for the plausibility of POS protocols is that these numbers are actually delivered to everyone participating in the protocol. In other words, the delivery of uniform randomness has to be guaranteed on the protocol level. Hence,to be a valid concept, especially from a formal academic viewpoint, Ouroboros must have a mechanism for generating and broadcasting “good” randomness. Furthermore, to be scalable, the generation and verification processes must be computationally inexpensive.Ouroboros solves these problems by embracing two well-known protocols from the field of distributed consensus: coin-tossing application of commitment schemes and verifiable secret sharing. Blending these two together produces a miracle: it creates a protocol for creating unbiased public randomness in a distributed adversarial setting with guaranteed output delivery. In layman terms, this means that Ouroboros:

- Generates provably random numbers;

- Guarantees that everyone will get them. Unchanged.

- Flexible and finance application-tailored scripting language: those who have experience with the Bitcoin scripting language know how draconian and inflexible it is, those who spent thousands of hours grinding through Solidity (the Ethereum scripting language), know how quickly it might become overly complex. Rigidity limits the number of applications; complexity limits the set of actors who are capable to work with the language and introduces larger scope for unintended errors and unnoticed bugs. To create a truly universal platform where those with bright ideas can compete for their share in the overall pie, one needs a simpler language whereby, simplicity would not come at the expense of the scope of application. Plutus is a general purpose Smart Contract language developed by IOHK and implemented in Cardano.

The core idea is that any type of financial transaction can be decomposed into simpler ones. Therefore, all the wide variety of complex financial instruments is comprised of a much smaller set of “foundational elements” that create the entire transactional logic. Cardano is designed by matters of code and is set to follow best practices; its scripting language is tailored for financial applications: security and execution can be “extremely well understood”.

With a certain degree of abstraction, one can observe strong parallels between any financial derivative and most of the gambling applications: in essence these are just contracts between one or more parties where outcome is conditioned, in part, on a realization of a random variable. This leads us to conclude that Plutus is the best of kind natural fit for writing casino applications.

Cardano is scalable, secure, and complex yet elegant. The major takeaway is that designing a successful POS protocol requires solving the same problems that constrain the creation of provably fair on-chain casinos. With Cardano as a backbone, Spade is set to become the best of its kind.

Our claims don’t require you to blindly trust us: all the results we rely on are proven with academic rigor and can be accessed by anyone on the ever-growing library of academic papers maintained by the IOHK foundation. Our competitors can appeal to the crowd stating that their protocol is unique, efficient and practically difficult to manipulate. Believing this implies having faith in their team: all the existing projects are either work-inprogress or completed, but centralized. All the results we rely upon are established with mathematical rigor and academic formalism by those for whom developing cryptography as a science is a profession, and state of the art code is an everyday tool.

The Spade Protocol

Before delving deeper into the mechanics of the SP8DE protocol itself, we opt to give a brief overview of the Cardano blockchain and, in particular, the Ouroboros protocol that underpins it. As mentioned above, Ouroboros is the first provably secure POS protocol. All POS protocols rely heavily on the miner selection process whereby a participant is selected at random to sign a block of transactions. In essence it is a POW system without the anchor to the real world — that of processing power. A precondition for an effective POS protocol is the ability to select the next ‘miner’ (or minter using the POS jargon) randomly with the uniform probability which is proportional to one’s stake in the system. The uniform nature of the probability distribution is an essential element: if it can be skewed or biased by any protocol participant, the security is compromised rendering the protocol useless.

At the heart of Ouroboros is the so-called Follow-The-Satoshi (FTS) procedure. Its essence is simple: assuming input of the uniform randomness, FTS is guaranteed to select a stakeholder with the uniform probability proportional to the number N of coins (or satoshis) one possess relative to the total number of coins in the system. In short, FTS does the job: it possess the qualities required to make an effective POS protocol. But, as always, there is a catch: FTS assumes input of ‘proper’ randomness. But where does it come from? Before answering this question, let us lead your through the mechanics of FTS procedure itself: it will prove useful later on.

The FTS proceeds along the following steps:

a. The fresh randomness is injected into the system;

b. It is used to ‘pick’ a single satoshi, the smallest unit of account in the system, an analogy to cent for US dollars;

c. All satoshis have ids. The state of the protocol determines which user (determined by the wallet id) was the last one to hold the satoshi selected;

d. This user becomes the ‘leader’ or in other words is entitled to sign a block

This simple procedure satisfied the required qualities of the protocol: assuming the input of unbiased randomness, it will select a stakeholder with the probability proportional to one’s stake in the system. Injecting ‘good’ randomness into the protocol is another important concern. FTS assumes input of good randomness, but in order for the protocol to work this randomness needs to be generated on-chain. At this point it is important to highlight the similarity of the design challenge that faces the POS protocols and onchain gambling applications: both of them require on-going inputs of unbiased distributed randomness.

Ouroboros employs the Fair Coin Tossing (FCT) procedure to generate randomness. This procedure is a known result in the field of academic and applied cryptography. It was first coined over 30 years ago and its mechanism is well studied and understood and is, thus, very efficient. The idea is that multiple entities participating in the protocol exchange ‘messages’ (the so-called commitments) that are encrypted by the sender and therefore are not known up-front by the receiver.

When opened (by exchanging the keys) and combined, these messages produce an output that cannot be known a priori and neither can be manipulated by those participating. One problem that remains is the possibility of one of the parties aborting the protocol by not sending the key to one’s message. In the Ouroboros protocol this issue is solved by employing yet another protocol that is called Publicly Verifiable Secret Sharing (PVSS) PVSS basically ensures that (given the honest majority) the message is delivered to everyone participating even if a malicious party chooses not

Token Utility

Software license

Getting access to the universe of applications just requires you to own the native token of our system, SPX.

Gaming Chip

Betting within Sp8de ecosystem is done only using SPX. By owning SPX, you share a part in protocol’s success.

Royalties

SPX is used to reward the developers fairly on the protocol level.

Wallet

The Search Engine of Gaming

Spade is a platform for developing decentralized casino applications.

Inspired to Create

Spade is decentralized marketplace for gaming with no frictions and no barriers to entry.

White Noise Powered Fairness

Voting mechanism is implemented on the protocol level: the rating of an application reflects the true consensus of the stakeholders and is immutable.

Legally Complient

Spade is intended to be fully compliant with all the required regulations.

Blockchain

Decentralized 3.0

The backbone of Sp8de, the Cardano blockchain is the first Proof-Of-Stake protocol without security compromises.

Scalable and Efficient

Tens of thousands of transactions per second: no user experience constraints.

Sp8de Smart Contracts

Smart-Contracts scripting language that was specifically designed for this.

TOKENS DISTRIBUTION

Sale

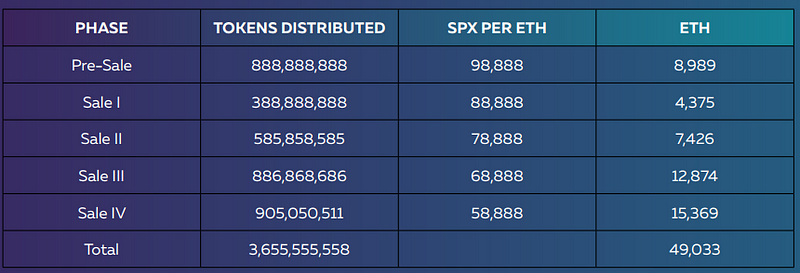

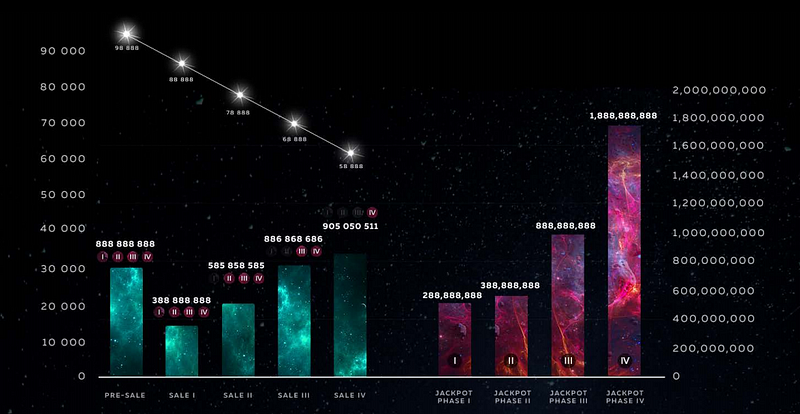

The entire token distribution will be 8,888,888,888 of which 3,655,555,558.4 (41.125%) will be in the form of token sale and 3,455,555,552 (38.875%) will be given as a jackpot to those who have participated in the “token sale” rounds. The rest of the tokens 1,777,777,778 (20%) will remain with the team for the purposes of marketing, advisory, and further development of the project (see the Token Proceeds Utilization section for further details on the use of the proceeds from the token distribution). From Table 2 it becomes clear that the SPX tokens received per ETH are decreasing after each sale while the tokens distributed are increasing following the PreSale stage. A soft cap of US$4,000,000 (four million) is set and the hard cap is ~ 49,033 ETH.

The token sale will take place in four rounds and the amounts in each round are as follows:

Jackpots

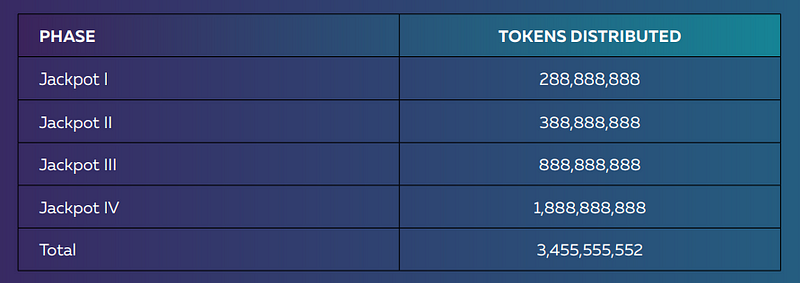

Everyone who participated in the token sale will be eligible to receive tokens during the jackpots. Table 3 outlines the jackpot distribution schedule:

Distribution Schedule

The token distribution begins on Monday, January 08, 2018 and ends on Sunday, March 11, 2018 and is scheduled as in the manner illustrated in Table 4 below. The Pre-Sale lasts for 24 days while each Sale phase will be seven days followed by a Jackpot that is distributed entirely within a single day after every Sale. A graphical illustration of the entire SPX distribution can be seen in Figure 2 below.

We believe that a true decentralized gaming platform has to be true to the casino spirit even in the design of

its fundraising campaign.

its fundraising campaign.

The ICO itself is divided into five stages: the pre-sale and four sale rounds. Each of the stages differs along

several important dimensions:

several important dimensions:

1. the number of tokens available,

2. the price of each token,

3. the likelihood of winning the lot that each token brings to its holder, and

4. the number of lots we have reserved for participants.

2. the price of each token,

3. the likelihood of winning the lot that each token brings to its holder, and

4. the number of lots we have reserved for participants.

The first two of these are conventional in the industry: the earlier birds get better prices. Points 3 and 4 are unique to Spade. Each sale round after the pre-sale is followed by a ‘jackpot round’ whereby a limited number of lots are randomly distributed among the token holders. These are illustrated as four bars on the right.

TOKENS DISTRIBUTION

The amount of SPX received for one ETH falls after each Sale round and in this way SPX is the cheapest during the Pre-Sale.

SPX per ETH

The amount of SPX distributed during each sale increases steadily after the Pre-Sale. The Jackpot amounts also increase in similar fashion but at much greater rate.

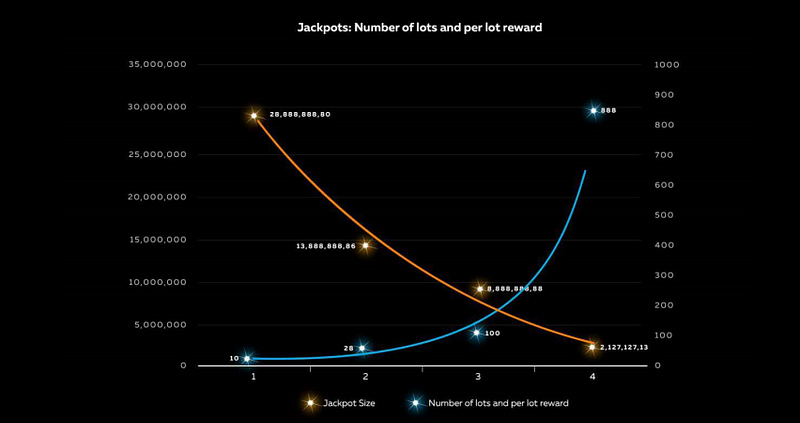

Participants in the earlier jackpot rounds have small chance of winning large lot, while those participating later have higher chance of winning, but are rewarded with smaller lots.

This shouldn’t discourage late participation: the largest combined pool of prize tokens is played during the fourth jackpot round. In addition, earlier contributors participate in more jackpot rounds.

So, those participating in the earlier jackpot rounds have small chance of winning large lot, while those participating later on have larger chance of winning, but are rewarded with smaller lots. In addition, earlier contributors participate in more jackpot rounds: e.g. sale I investors try their luck four times, while those entering at sale III can only participate in two jackpots. This shouldn’t discourage late participation: the largest combined pool of prize tokens is played during the fourth jackpot round. For every lot we run a procedure which randomly selects one token out of those already issued. The holder of this token becomes the winner of the lot.

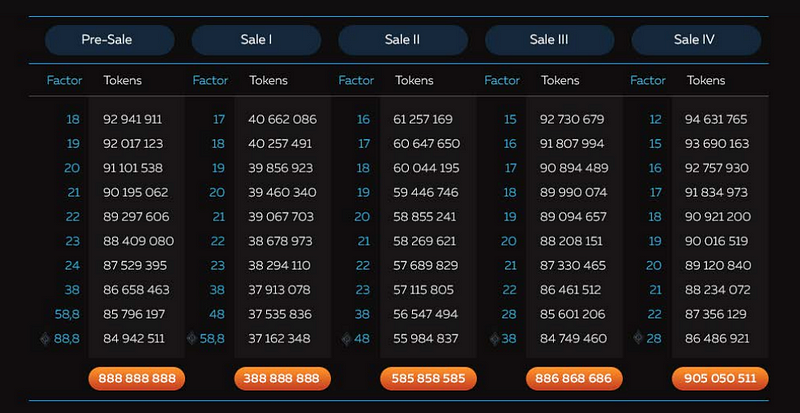

Each token being sold has a specific factor attached to it, the jackpot factor. The likelihood to win a lot is proportional to this factor. Mind, that jackpot factors are ordered: even within one sale round, earlier contribution is rewarded with more ‘powerful’ tokens. The distribution of these factors for every round is shown in the table below.

How Jackpots work...

Each token being sold has a specific factor attached to it, the jackpot factor. The likelihood to win a lot is proportional to this factor.

Mind, that jackpot factors are ordered: even within one sale round, earlier contribution is rewarded with more «powerful» tokens. The distribution of these factors for every round is shown in the table above.

Unpurchased Tokens Allocation

There is a possibility that some part of every token Sale will remain unpurchased. As illustrated in Table 6 the majority of the tokens that remain unsold will be automatically distributed among the Jackpots, increasing the number of tokens to be received by the participants in every Sale. If any tokens are allocated to the Spade Foundation they will be used for further development and promotion of the project

Token Proceeds Utilization

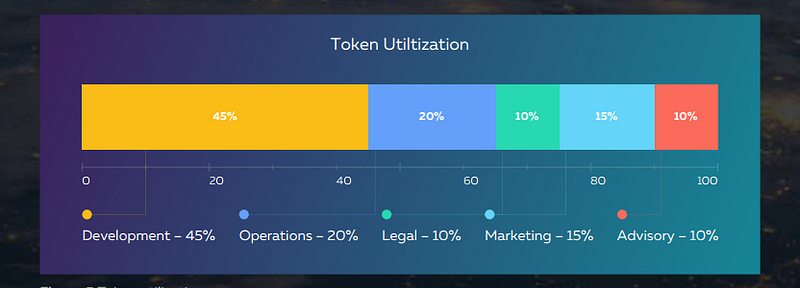

The proceeds of the token sales as well as the tokens that remain in possession of the team will be used to promote and develop the project as outlined in the Road Map section of this paper. In the figure below, we show how the proceeds will be utilized. As we have shown earlier Spade is development intense, therefore we allocate the majority of the proceeds to development and operations as we believe that proper management and highly skilled developers are in the core of the success of this project. Furthermore, when needed the tokens allocated to the Spade Foundation and the team might be used for further promotion and as part of an incentives scheme.

Road Map

Team & Advisors

Alexey Kashirsky

CEO & Co-Founder

IT Mining Engineer graduate the Moscow State Mining University MBA program of Mining Nitu “MISiS” Adviser to the General Director of NP “Miners of Russia” and an adviser to the Russian Academy of Natural Sciences, in the association “Industrial minerals”- an assistant to the president

Mikhail Krapivnoi

CIO & Co-Founder

ex Ceo of Man & Machine

A robotics research Company Multi Entrepreneur Champion in Online Poker and Chess Member of the AI Research Association Blockchain Evangelist And just a cool guy.

ex Ceo of Man & Machine

A robotics research Company Multi Entrepreneur Champion in Online Poker and Chess Member of the AI Research Association Blockchain Evangelist And just a cool guy.

Evgeny Borchers

CVO & Co-Founder

A visionary,

experienced business expert focused on cryptocurrency investing, Fin-Tech, and affiliate marketing since 2013. Co-founder of a number of Fin-Tech projects, the most recent one of which DCEX, a digital currency exchange.

experienced business expert focused on cryptocurrency investing, Fin-Tech, and affiliate marketing since 2013. Co-founder of a number of Fin-Tech projects, the most recent one of which DCEX, a digital currency exchange.

Alexander Baykiev

CMO & Co-founder

Responsible for the digital marketing, media communications, and creative content development to develop and sustain the brands of a number of businesses.

Artemy Zorin

Advisor Graphics Design

Interactive designer user interface and visual and visual style for web and mobile applications. Visual design and branding manager, head of design department, „Yodiz“ studio. Cool Dude. Loves Blockchain.

Alexander Uglov

Advisor Marketing

Blockchain-evangelist, visionary. Has experience of staging in several projects C(SONM, Humaniq, etc). CEO of the Russian Media digital agency. 8 years’ experience in Internet marketing and creating web services.

Norman Chou

Advisor Strategic Business

Norman Chou is an blockchain enthusiast and believes hat blockchain will impact esociety in the most positive ways. worked for technology companies including CDW Dell, and EMC

Lyubomir Serafimov

Advisor Operations

Served as a risk manager in a number of firms in the financial services industry, built risk systems and processes supporting the liquidity provision of cryptocurrency exchanges, and developed arbitrage trading strategies. An economic advisor to the Open Trading Network project and a Chief Strategy Officer at a digital currency exchange — DCEX.

Media

Further Information:

Bitcointalk Profile Link:

https://bitcointalk.org/index.php?action=profileETH address:

0x249A78DFC8674236CD0E7f1B81C7cd69822B2692

Tidak ada komentar:

Posting Komentar